Clearly, open blockchains are available to anyone who has an Internet connection. Private blockchains are typically used in enterprise solutions to solve business cases and underpin corporate software solutions. The consortium blockchain is a system that is ‘semi-private’ and has a controlled user group, but works across different organizations.

There are many benefits to consortium systems, and many blockchain platforms are setting themselves up as a backbone for these cross-company and cross-discipline solutions. A blockchain consortium of like-minded companies can leverage information to improve workflows, accountability, and transparency.

Article Contents

Shared Platforms

Fully open blockchains with open-source development models are designed to leverage talent from many different people around the world, and use a wide-ranging user base to have maximum decentralization. You have a more trusted consensus when you have a large group with varied interests, and no central authority to override the group.

Private blockchain systems, by contrast, are not very decentralized, because they are controlled by a company and assigned a set user base. There’s less trust in a consensus of users when the central authority (in this case, the company) chose the users.

Consortium blockchain vs. private blockchain is a sweet-spot between fully open, decentralized systems and fully centrally-controlled. There’s more likely to be a trusted consensus, as multiple organizations have a stake in the outcome.

Shared Resources

Instead of each company building their own solution from scratch, by being part of a blockchain consortium, they can share development cost and time with other organizations. This can lead to shorter development times and economies of scale, which will allow smaller organizations to take advantage of the same systems as larger ones.

These groups of organizations identify common problems that each of their businesses needs to solve, and each contributes to the solution. Specialized industry consortiums are the end result, or more recently — even interfacing business disciplines are working together. An example would be a manufacturer working with logistics companies: two business disciplines part of one supply-chain blockchain consortium.

Software Platforms

Quorum (based on Ethereum), R3 Corda and Hyperledger have emerged as some of the most popular blockchain development platforms. Each is suited to different industries and types of solutions, and developers are working with them around the world. This combines the best of open-source development with the semi-private nature of enterprise-level systems.

Hyperledger Fabric is the result of a consortium of large companies that cross disciplines and industries — from finance to logistics to manufacturing to banking. Companies such as IBM, SAP, Daimler, Fujitsu and Intel all collaborated on the project.

It has created an ‘open-source’ enterprise-level framework to build business solutions on, backed by all the consortium members. This type of collaboration is unique in what is normally a very closed-off and competitive corporate environment.

Financial Business Consortiums

While the above examples are of a technology consortium building a platform rather than a solution, there are also business consortiums. Back in early 2017, several global financial institutions got together to form the Digital Trade Chain.

Members included such high-profile companies as Deutsche Bank, UniCredit and Rabobank. By late 2017, they had launched we.trade, a financial service blockchain solution available to anyone who wanted to join. The wide range of companies involved makes the system work more like an open blockchain, even though users only come from within member organizations.

By leveraging resources across multiple banking firms, they were able to create a blockchain-based system quickly, going live in less than a year. By opening up the solution to new users, they are increasing the functionality and trust level of their consensus algorithm.

Other Industries Forming Consortia

While there’s no definitive blockchain consortium list, a little research will turn up suitable ones for your industry. Recently, for example, 94 companies signed up to be a part of the IBM/Maersk blockchain-based supply chain initiative.

Healthcare is another industry that is pooling resources to solve industry-wide issues and improve efficiency, speed and security of patient data. Hashed Health is a technology consortium that is working on creating platforms that will work across disciplines to service those goals.

Power In Numbers

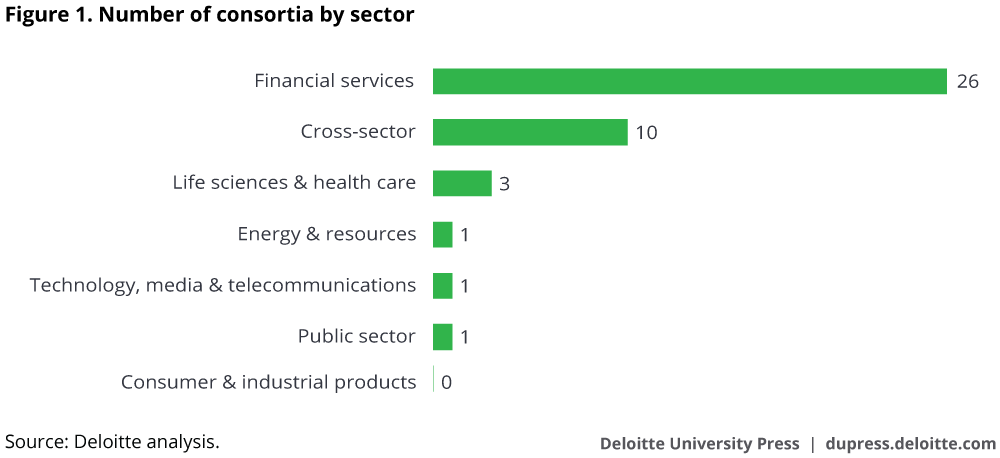

While the majority of consortia so far are from the financial sector, many other industries are joining in to work on blockchain-based systems and reap such benefits as shared resources, decreased development time and increased consensus trust.

The rapid growth of these different consortia shows just how powerful the sharing of resources can be, and why it’s worth joining a consortium if you’re thinking of adding blockchain-based systems to your business in the future.

Did you like the article? Give your rating

Blockchain Insights

Join our mailing list to receive OpenLedger Insights publications weekly.

Thanks! Please check your inbox to verify your email address.

By clicking “Subscribe”, you’re accepting to receive newsletter emails from OpenLedger Insights every week. You can easily update your email or unsubscribe from our mailing list at any time. You can find more details in our Privacy Policy.